Inside Kremlin's trap: Why global oil crisis won't bail out Russia

Problems with the Russian budget are mounting (Getty Images)

Problems with the Russian budget are mounting (Getty Images)

The escalation in the Middle East has temporarily brought Russia additional oil and gas revenues. But even the sharp spike in oil prices has failed to halt the growth of Russia’s budget deficit. Military spending and attacks on oil infrastructure are increasing pressure on the Kremlin’s financial system.

Read the RBC-Ukraine article to find out why Russia’s budget deficit is growing despite the sharp rise in oil prices.

Key points:

- Russia's budget deficit continues to grow despite high oil prices

- Rising military and social spending is outpacing oil and gas revenues

- Attacks on Russia’s oil infrastructure are hampering exports and refining

- The Kremlin is preparing to seek new sources of budget revenue, from raising taxes to cutting social spending.

The Russian budget, whose revenues began to decline sharply at the end of last year due to US sanctions, has cemented this trend this year.

According to Ukrainian intelligence, the budget deficit rose to $69.9 billion in January-February 2026. This is one and a half times higher than the Ministry of Finance’s estimate ($43.3 billion) and already exceeds the annual target of $50.5 billion.

By the end of April, the deficit had already reached $78.4 billion. Expenditures increased by 15.7% compared to last year. Funding for military and social programs, as well as for certain sectors of the economy, has increased.

Revenues fell by 4.5% to 11,721 billion rubles. At the same time, the economic growth forecast for 2026 has been lowered from 1.3% to 0.4%.

Russia’s Ministry of Finance acknowledges the deficit as high, but in an attempt to downplay the situation, officials state that it aligns with the target parameters for the structural deficit.

The increase in the deficit is explained by pre-emptive funding of expenditures. This means that money is being spent in advance from the budget allocated for the second half of the year.

However, the budget deficit could have been even higher had it not been for the escalation of the situation in Iran. It has radically changed the geopolitical and economic landscape worldwide.

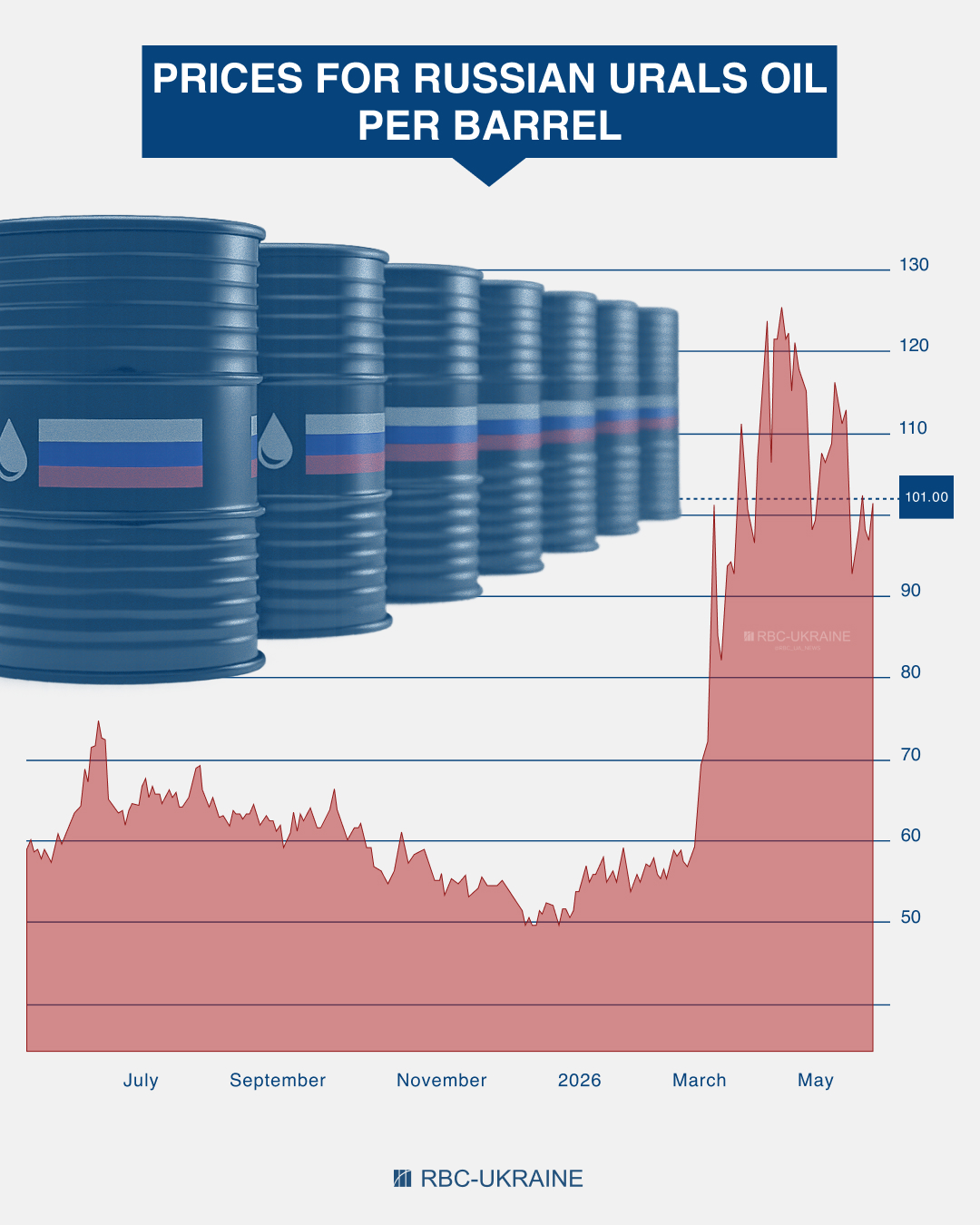

The oil crisis caused by the blockade of the Strait of Hormuz led to a sharp rise in energy prices. The price of Brent crude exceeded $100, and on some days even $120 per barrel.

The price of Russian Urals crude oil more than doubled compared to the start of the year. At the height of the conflict in Iran in early April, its price soared to $124 per barrel.

Oil price data based on IEEFA materials

Oil price data based on IEEFA materials

Europe, primarily France, Spain, and Belgium, increased imports of Russian LNG by 6.9 billion cubic meters (16–17%) in the first quarter of 2026, according to the IEEFA.

China and India sharply increased their purchases of Russian oil to compensate for supply disruptions from the Middle East.

According to the latest data, Russia’s daily revenue from oil exports amounts to €374 million, and from gas, €78 million.

Rising oil prices have not significantly helped Russian budget

Undoubtedly, rising oil and gas prices and increased import volumes have had a positive impact on Russia’s revenues. However, in January–April of this year, they were still 38.3% lower than during the same period last year, totaling 2.298 trillion rubles.

In fact, Russia is currently reaping windfall profits from oil and gas exports. But these are not enough to cover the increase in military and social spending.

To cover Russia’s budget deficit, oil prices must remain at today’s levels until at least the second quarter of next year, according to financial analyst Andrii Shevchyshyn.

"The Russian current budget deficit for the first four months is 5.9 trillion rubles. To cover just this deficit, oil prices would need to remain at current levels for 8–11 months. But I don’t believe that will happen," he notes.

The second scenario is that oil prices will rise to $200 per barrel and remain at that level for 4–5 months. But Shevchyshyn is convinced this is practically impossible. Even the current high prices, if sustained for several more months, could lead to a global crisis and a drop in oil prices.

A crisis leads to inflation, devaluation, a contraction in production, and, as a result, a reduction in demand for oil, which causes prices to fall.

Shevchyshyn believes that in order to fill the budget, a windfall tax could be introduced for companies in the oil and gas sector, given the rise in oil and gas prices.

"Roughly speaking, this could potentially yield an additional 25–30%. The potential for additional budget revenue is $7.7 billion per month," the expert says.

In March, Putin did indeed instruct the government to explore the option of a windfall tax. But this tax, at least for now, was not intended for companies in the oil and gas industry. It may affect steelmakers and gold miners.

An attempt to implement a similar measure was already made in 2023, when a one-time levy was introduced in Russia. It brought an additional 319 billion rubles to the budget.

Former advisor to the President of Ukraine, Oleh Ustenko, attributes the relatively weak impact of rising oil prices on Russian budget revenues to the fact that the peak prices did not last long.

"They lasted from a few days to 1-2 weeks. The weighted average price, however, was still below $110," he notes in a comment to RBC-Ukraine.

Ukrainian strikes, which intensified precisely at the start of the war in Iran, played a more significant role in reducing potential revenues.

Fire at the Lukoil refinery following an attack by Ukrainian drones (photo: Unmanned Systems Forces of the Armed Forces of Ukraine)

Fire at the Lukoil refinery following an attack by Ukrainian drones (photo: Unmanned Systems Forces of the Armed Forces of Ukraine)

The Ukrainian Armed Forces have been targeting port infrastructure used for the export of oil and petroleum products. On some days, oil exports from these ports have dropped by 40% due to strikes on oil terminals and oil transshipment facilities. However, these facilities are being restored fairly quickly.

Strikes are also being carried out on key oil pumping stations. Putting them out of commission blocks the loading of oil onto tankers. In other words, oil can be delivered to the port, but it cannot be pumped into a tanker. In effect, such shelling also reduces the physical volume of potential exports.

As a result, oil exports did increase, but the revenue from them was not as high as it could have been without the strikes on infrastructure. Moreover, discounts for India and China increased, which reduced the potential margin for Russia.

Meanwhile, exports of petroleum products fell by 10%. Here, the financial losses were more significant due to higher prices for refined petroleum products compared to crude oil.

As a result, in budget revenues, the losses from the decline in petroleum product exports were offset by increased revenues from crude oil sales.

Budget deficit will grow

The Ukrainian Armed Forces are targeting not only the port infrastructure that facilitates the export of oil and petroleum products, but also refineries and oil storage facilities. This creates problems for oil refining and could lead to a reduction in oil production, Oleh Ustenko believes.

"If there is no way to transport oil to transfer points or for refining, then companies will simply have to cut production," Ustenko notes.

The latest statistics confirm that the process has already begun. By the end of April, production had fallen by 5% compared to April, to 9.29 million barrels per day.

"Russian companies are in a stalemate. There is oil in the ground, but there is no point in extracting it. Therefore, budget problems will grow depending on the directions in which the Ukrainian Armed Forces’ attacks continue," Ustenko notes.

He is confident that port infrastructure, which facilitates the export of oil and petroleum products, as well as refineries and oil storage facilities, will remain targets. It is precisely this comprehensive approach that will ensure the maximum reduction in Russia’s revenue from oil imports through military means.

But the collapse of the Russian economy will not happen anytime soon, Ustenko is certain. The Kremlin still has enough resources in reserve to keep its military machine running.

"Moscow solves budget problems quickly and without unnecessary discussion. The Duma has already been forced to vote for raising the VAT to 22%. If budget funding problems escalate, they will start cutting spending on the social sector. And if discontent arises within the country, they will deploy the repressive apparatus. Spending on security forces there has been increasing since 2023," notes Oleh Ustenko.

The Kremlin fully understands that the situation is escalating and that the growth in oil revenues is temporary.

Putin has already publicly stated that Russian companies and the government should exercise caution when using the windfall profits from rising oil prices.

Quick Q&A

— Why isn’t the rise in oil prices saving the Russian budget?

— Even after the sharp rise in oil and gas prices, Russia’s revenues are growing more slowly than its expenditures. The main reason is record spending on the war, the security apparatus, and economic support.

— How has the war in Iran helped Russia?

— The crisis in the Middle East has driven up global oil and gas prices. Russia has temporarily increased its revenues from energy exports, while China and India have stepped up their purchases of Russian oil.

— Why was the effect of high oil prices limited?

— High prices did not last long, and Russian oil continues to be sold at a discount. Additionally, exports are affected by strikes on oil infrastructure and logistical problems.

— How are Ukrainian military attacks affecting Russia’s oil revenues?

— Strikes on refineries, oil depots, ports, and transshipment facilities are complicating oil exports and refining. This reduces Russia’s potential revenues and creates risks of a decline in production.

—How might the Kremlin cover the budget deficit?

— The Russian government can raise taxes, increase pressure on businesses, expand domestic borrowing, and cut some social spending.

— Is a collapse of the Russian economy possible in the near future?

— Despite the growing budget deficit, the Kremlin still has financial reserves and tools to support the military economy.