Risk of euro zone crisis rises due to French elections results - Reuters

Photo: The euro could be in crisis (Getty Images)

Photo: The euro could be in crisis (Getty Images)

The risks of a new crisis in the single currency area, similar to the collapse that occurred more than a decade ago, are growing. But conditions may not yet be ripe to trigger it, according to Reuters.

The main fear at the moment is that France, where the far-right National Rally party is winning the first round of early parliamentary elections, could enter a period of extreme political instability and financial waste. This could lead to a sharp rise in French government bond yields.

Other heavily indebted eurozone countries, especially Italy, could suffer from contagion. The single currency would then be on the verge of collapse. France and Italy are much larger economies than Greece and other eurozone countries that were at the center of the last crisis.

But this scenario does not seem inevitable, as Jordan Bardella, the far-right candidate for Prime Minister, is softening his party's fiscal promises. The National Rally is hoping to win the French presidential election in 2027, and it would be foolish to undermine its credibility by provoking a financial crisis beforehand.

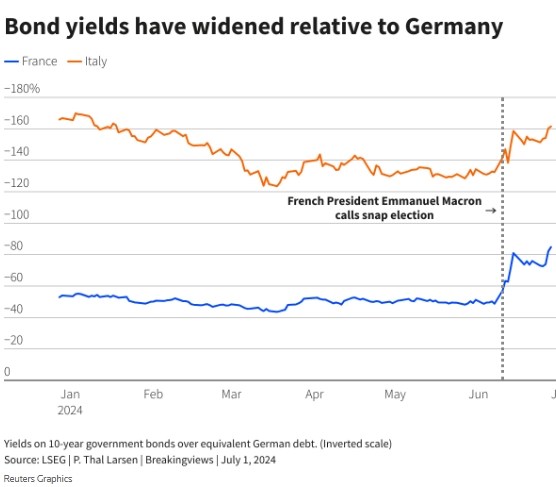

Investors are not overly concerned. Since President Emmanuel Macron announced his election, the yield differential between French and German 10-year government bonds has widened, from 49 basis points to 85 basis points. Italy's reaction was limited, with the spread of its bond yields over German bonds widening to 162 basis points from 133 basis points. Back in 2011, when Silvio Berlusconi was Prime Minister, the gap was 560 basis points.

Photo: Reuters

However, the medium-term prospects for the single currency are worrying. High debts, urgent spending needs, and low growth in many countries at a time of rising nationalism and geopolitical conflict pose challenges, Reuters writes.

Lines of defense

The eurozone has the means to protect itself from the financial crisis. If a country's bond yield spreads widen sharply, the European Central Bank can step in and buy its debt. Its Transmission Protection Instrument (TPI) is designed to counteract unreasonable, disorderly market dynamics.

The central bank is much more prepared to intervene than at the start of the last euro crisis. It was only after Mario Draghi became its president and promised to do whatever it took that the ECB developed a tool to combat market chaos in 2012.

The ECB says it will only come to the rescue if a country pursues sound and sustainable fiscal and macroeconomic policies. This could leave a delinquent government face-to-face with debt investors, as was the case with Greece until it adopted a responsible budget program in 2015.

Mathematics of debt

One of the differences between today's situation and the euro crisis is that interest rates are now higher. Therefore, servicing the public debt is more expensive.

According to the International Monetary Fund, last year Italy's borrowings amounted to 137% of national income, while France's debt was 111%. Meanwhile, the budget deficit of the two countries was 7.2% and 5.5% of GDP, respectively.

The European Commission concluded last month that both countries - along with seven others that use the single currency and three that do not - are running excessive deficits. In the coming months, it will try to persuade each of them to reduce their debt ratios as part of the union's excessive deficit procedure. France and Italy may have to tighten fiscal policy by 0.5% and 0.6% of GDP, respectively, if they have a maximum of seven years to adjust.

Politicians will be reluctant to cut public spending or raise taxes, as this would undermine their popularity and slow economic growth. But they may agree on a deal with the European Commission. If so, the markets should remain calm for now.

The problem is that, according to IMF forecasts, debt ratios will continue to rise, reaching 145% of GDP in Italy and 115% in France by 2029. Thus, borrowing ratios will remain high even after some fiscal optimization.

It will also be difficult to contain the deficit. In the coming years, all European governments will have to spend more money on defense, climate change, and population aging.

Eurozone countries will not be able to simply grow out of their debts. The French economy will grow by an average of just 1.3% over the next six years, while Italy will only be able to grow by 0.6%, according to the IMF.

Their task will become even more difficult if the geopolitical situation worsens. The creeping cold war between China and the United States and the resulting fragmentation of the global trading system is already holding back the global economy. If Donald Trump returns to the White House and follows through on his promises to impose tariffs, economic growth will take another hit.

The EU could counter some of these forces if it could boost productivity and investment. It could strengthen its single market, which currently excludes energy, capital markets, and digital communications. It could adopt a targeted EU-wide industrial policy, funded from the central budget, to keep up with China and the US, which use subsidies to prop up their companies.

Draghi will soon develop a project in this direction. The problem is that this policy needs more unity. Nationalist politicians, whose numbers are growing across the EU, will not want to accept them. Thus, the eurozone seems doomed to slow growth and high debt. "As more dry tinder accumulates on the forest floor, the risk of another blaze keeps growing," Reuters writes.

The far-right National Rally won the first round of parliamentary elections in France on 30 June. President Emmanuel Macron's party came in third place.

The second round of elections will be held on 7 July. Candidates who received at least 12.5% of the vote in the first round will take part in it.